Financial Literacy For Kids

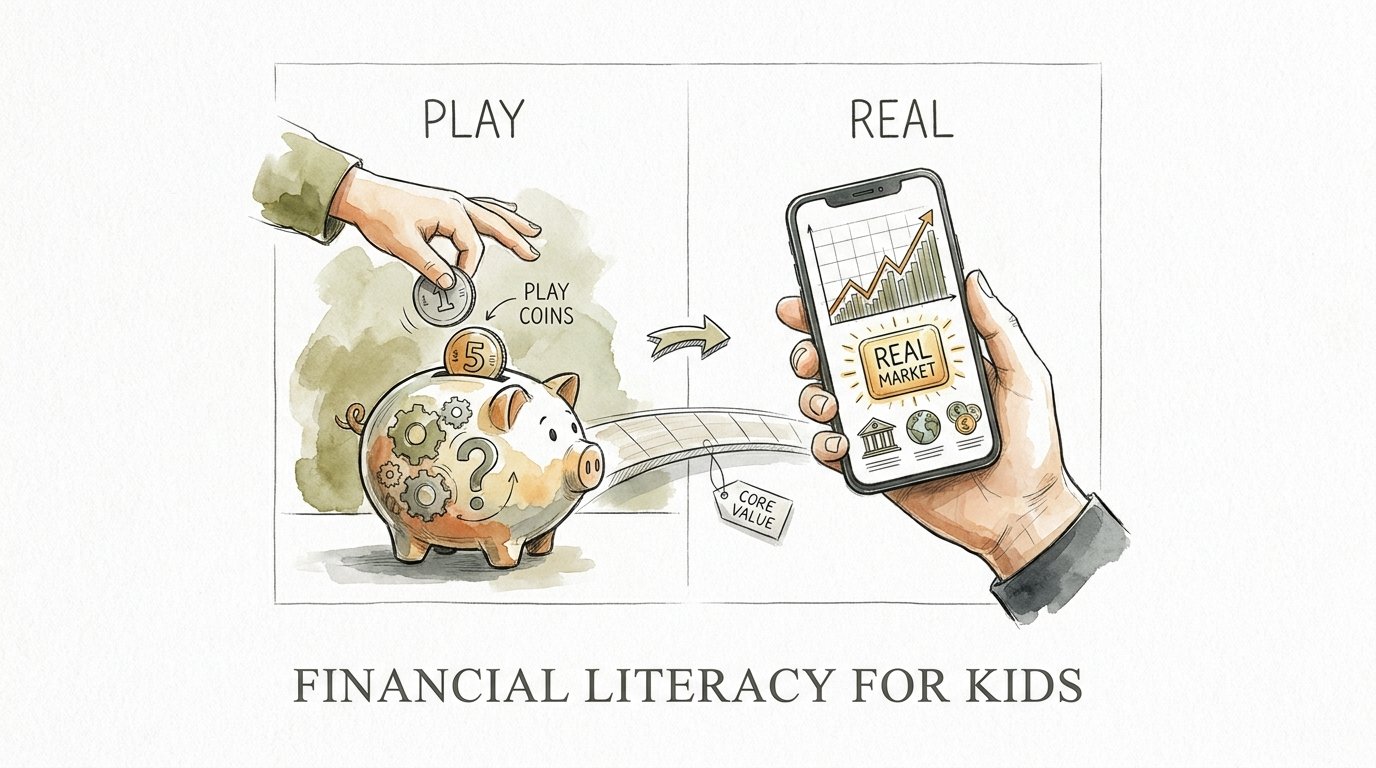

Why does a child care more about 50 cents than 50 plastic tokens? Because reality has weight that play-time lacks. We shelter kids with plastic ‘fake’ versions of the world and wonder why they aren’t engaged. When you give a child real currency, the math becomes an emergency—they have to get it right. This ‘exposure’ to the real market builds cognitive resilience that a classroom simulation never will.

Teaching children about money is often treated as a chore or a theoretical lecture. We hand them colorful paper or plastic coins and expect them to understand the global economy. It doesn’t work. True understanding comes from friction, risk, and reward.

Real-world application is the only way to bridge the gap between “counting” and “comprehending.” This guide explores how to move past simulations and into a functional home economy that prepares children for the complexities of adulthood.

Financial Literacy For Kids

Financial literacy for kids is the ability to understand and effectively use various financial skills. It is not just about knowing how to count coins or put money in a piggy bank. It involves a deep understanding of personal financial management, budgeting, and the concept of “opportunity cost.”

In the real world, every financial decision is a trade-off. When we use PLAY COINS, we remove the weight of that trade-off. If a child “spends” a plastic token on a fake apple, they lose nothing of value. If they spend fifty cents on a candy bar, they lose the ability to buy a sticker later.

Financial literacy exists to provide children with a toolkit for independence. It is used every time a child decides to save for a long-term goal or chooses a generic brand over a name brand to save money. By introducing these concepts early, we move from theoretical “math problems” to practical “life solutions.”

The Mechanics: How a Real Market Works at Home

Moving from a passive allowance to a “Real Market” system requires a shift in how you view household chores and rewards. Experts often suggest a “Commission” system rather than a flat allowance. This mirrors the real-world earning structure where effort correlates with income.

The Commission System

Create a list of “extra” tasks that go beyond daily responsibilities. Daily tasks like making the bed or clearing their own plate are “family contributions.” These are unpaid. Commissions are for tasks that add value to the home, like washing the car, weeding the garden, or organizing the pantry.

Assign a clear dollar value to each commission. This allows the child to calculate their potential earnings. They aren’t just waiting for a Friday handout. They are actively deciding how much work they are willing to do for the lifestyle they want.

The Home Economy Setup

A more advanced version involves a “Home Economy.” In this system, children earn a larger “salary” for their main “job” (being a student or helping with major chores) but also face “expenses.” They might pay “rent” for their room or a small “utility fee” for high-speed internet.

While this sounds harsh, it is highly effective. It teaches them that “Gross Pay” is not “Net Pay.” When they see $10 in their hand but realize $2 must go back to the “Bank of Mom and Dad” for their phone bill, the concept of budgeting becomes a survival skill.

The Psychological Benefits of Real Stakes

When a child has “skin in the game,” their brain functions differently. Real stakes trigger a higher level of cognitive engagement. They become researchers. They compare prices. They look for discounts.

Building Cognitive Resilience

Handling real money builds resilience through “micro-failures.” It is much better for a child to lose $10 on a poorly made toy today than to lose $10,000 on a bad car loan at age twenty-five. These early “abrasions” guide their discovery of value.

Developing Delayed Gratification

One of the greatest predictors of adult success is the ability to delay gratification. A real market environment forces this. If they want the $50 Lego set, they have to resist the $2 candy bar for twenty-five consecutive weeks. This builds a mental “muscle” that classroom simulations cannot replicate.

Challenges and Common Mistakes

The biggest challenge isn’t the child; it’s the parent’s consistency. If the “Bank of Dad” gives out “bailouts” every time a child goes broke, the lesson is lost. You must let the consequences land.

The Bailout Trap

When a child runs out of money and can’t go to the movies with friends, it hurts. As a parent, your instinct is to fix it. Do not. If you bail them out, you teach them that “risk” isn’t real. You teach them that there is always a safety net, which is a dangerous lesson for the real world.

Consistency in Payment

If you forget to “pay” commissions, the child loses motivation. The market must be reliable. If they do the work, the money must appear on time. If the system becomes erratic, the child will view it as a game rather than a profession.

Limitations: When the Method May Not Work

While real-world exposure is powerful, it is not a one-size-fits-all solution. There are realistic constraints that every parent should consider before implementing a full home economy.

Age and Cognitive Development

Children follow specific stages of cognitive development. A four-year-old may not understand that “rent” is a recurring expense. For younger children, stick to immediate “work-for-pay” transactions. The abstract concept of monthly budgeting usually requires the “concrete operational” stage, typically starting around age seven.

Socioeconomic Constraints

The ability to provide a commission-based system depends on the family’s extra budget. Not every household has $20 a week to spare for chores. In these cases, you can use “time currency” or “privilege points.” While not as heavy as cash, they still provide a measurable trade-off.

Comparing Methods: Play Coins vs. Real Market

Understanding the difference between these two approaches helps in choosing the right path for your family’s needs.

| Factor | Play Coins / Simulations | Real Market Exposure |

|---|---|---|

| Engagement | Moderate; treated as a game. | High; stakes feel personal. |

| Risk of Error | None; mistakes are easily reset. | High; mistakes result in lost value. |

| Long-term Retention | Low; lessons often remain theoretical. | High; visceral experience stays with them. |

| Complexity | Simple; easy to set up and drop. | Higher; requires ongoing management. |

Practical Best Practices

If you are ready to start, follow these actionable tips to ensure the system is effective and sustainable.

- Use the Three Bucket System: Encourage them to divide every dollar into “Spend,” “Save,” and “Give.” This teaches that money has multiple purposes, not just consumption.

- Let Them Make Mistakes: If they want to buy a $15 plastic sword that will break in an hour, let them. The sadness of the broken toy is a more powerful teacher than a thirty-minute lecture on quality.

- Match Their Savings: To encourage long-term thinking, offer a “Parental Match.” For every dollar they save for more than three months, you add 50 cents. This introduces the concept of an employer-matched 401(k) in a way they can understand.

- Use Digital Tools: As they get older, transition to apps like Greenlight or BusyKid. Real-world money is increasingly digital. They need to see a balance go down on a screen to understand the “invisibility” of modern transactions.

Advanced Considerations: Taxes and Interest

For older children or teens, the basics are not enough. You want to introduce “Advanced Market Variables” to further prepare them for adulthood.

The “Dad Tax” and Public Goods

Introduce a small, 5% “tax” on their earnings. Explain that this money goes into a “Family Fund” used for “public goods” like popcorn on movie night or new board games for everyone. This helps them understand that society requires shared contributions and that “Gross Income” is never what you actually take home.

The Power of Compounding

Show them the math of “Interest.” If they leave money in the “Family Bank” (a jar or account) and don’t touch it, pay them a monthly interest rate. Make it high—perhaps 5% per month—so they can see the growth happening in real-time. This “wow factor” is the best way to explain how wealth is actually built over decades.

Scenario: The $100 Skateboard Lesson

Let’s look at how this works in practice. Imagine ten-year-old Leo wants a $100 professional skateboard.

In a **Play Coin** world, Leo might do some fake chores, get “Leo Bucks,” and “buy” a picture of a skateboard from a chart. He learns nothing about the sweat equity required for that purchase.

In a **Real Market** world, Leo has to earn $100 in commissions. He realizes that at $5 per car wash, he needs to wash twenty cars. After five weeks, he has $25. He is tired. He sees a $10 video game on sale.

Leo faces a choice. If he buys the game, his skateboard is now three weeks further away. He chooses to skip the game. By week fifteen, he has saved enough. When he finally buys that skateboard, he treats it with immense care. Why? Because he knows exactly how many hours of car-washing it cost. That is “Skin in the Game.”

Final Thoughts

Financial literacy for kids is not a destination; it is a mindset. It is the transition from being a passive consumer to an active participant in their own life. By replacing “fake” tokens with real currency and real consequences, you give your child a head start that no classroom can provide.

The goal is to raise adults who are not intimidated by banks, budgets, or bills. You are building their confidence through competence. When they move out at eighteen, they won’t be surprised by the “real world” because they have been living in a microcosm of it for years.

Start small. Be consistent. Let them fail while the stakes are low. The resilience they build today will be the foundation of their success tomorrow. Experiment with different “commissions” and see how their engagement shifts when the money—and the math—becomes real.

Sources

1 golden1.com | 2 medium.com | 3 lemonadeday.org | 4 molentax.com | 5 ccu.edu | 6 tiempocapital.com | 7 bankofamerica.com | 8 bankofthejames.bank | 9 fermentingtofinance.org | 10 ameripriseadvisors.com | 11 lovetoknow.com | 12 moneytimekids.com | 13 myclassroomeconomy.org | 14 demmelearning.com | 15 substack.com | 16 finra.org | 17 penfed.org | 18 ramseysolutions.com | 19 abajourney.com